Master the concept of Deferred Revenue so you can use it on the job in Investment Banking, Private Equity, and Hedge Funds or Mutual Funds.

In this article, we will cover:

What type of transaction creates Deferred Revenue for a Business.

Why we record the Deferred Revenue Account on the Balance Sheet as a Liability.

How to record Deferred Revenue Journal Entries (Debits & Credits)

- The Impact of Deferred Revenue on the Financial Statements.

Examples of Deferred Revenue in Real Life situations.

Estimated reading time: 9 minutes

TL;DR

A Business records Deferred Revenue when a Customer prepays for future goods or services.

We record Deferred Revenue as a Liability because it reflects the obligation to deliver goods or services to a Customer in the future.

Why Does Deferred Revenue Matter?

Deferred Revenue (also called Unearned Revenue) is a critical concept to master if you are aiming for (or currently working in) Finance.

As you will see, we record Deferred Revenue to the Balance Sheet when a customer prepays in advance of receiving goods and services due to Accrual Accounting rules.

Need to Master Accounting for Interviews or the Job?

Check our Accounting Deep Dive Course

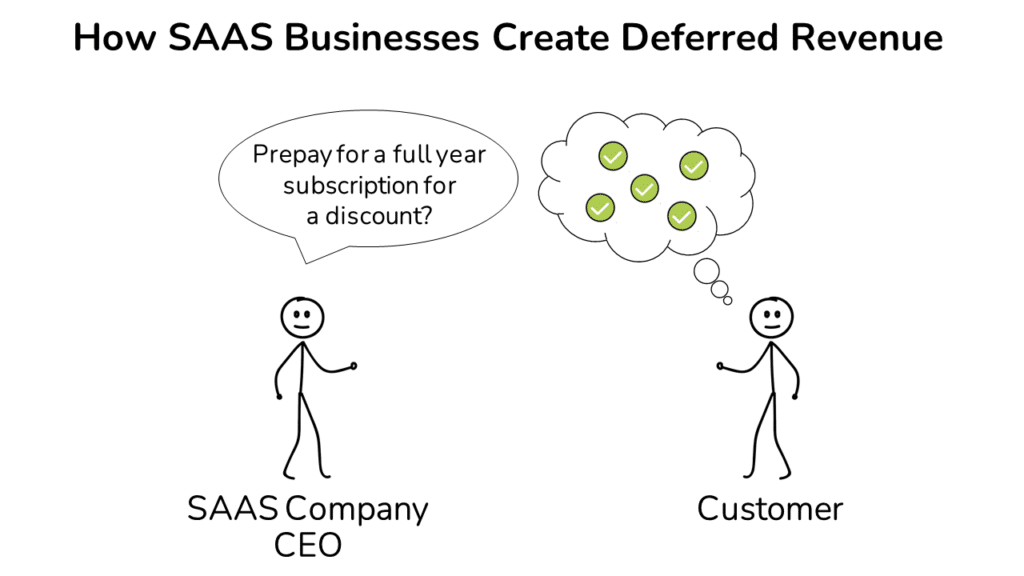

How does a Business Create Deferred Revenue?

Companies record Deferred Revenue when a customer pays in advance to receive future goods or services from a Business.

If you are thinking, ‘Why on earth would a customer make advance payments to a Business before receiving a Good or Service?‘, you’re on the right track.

Let’s look at an everyday example where we might prepay for a future service.

Deferred Revenue Example: Apple Music Subscription

To kick off our discussion here, Customers typically don’t pay ahead of time without some form of attractive prepayment terms.

In most cases, Customers agree to pay in advance because they receive a discount.

A great real-life example of this is paying in advance for a year-long subscription to a service like Apple Music (or any other subscription-based services for that matter).

For an annual subscription, a customer would normally pay $10 per month ($120 per year) for Apple Music.

However, if a customer is willing to pay for a full year in advance, the price is just $99.

But how do we record a transaction when a customer prepays for future goods or services?

Why Don’t We Record Revenue If The Company Receives Payment?

The key thing to understand about the transaction in the previous section is that we can’t record the entire $99 as Revenue on the Income Statement upon advance payment by a customer.

Per US GAAP (Generally Accepted Accounting Principles), we don’t record Revenue on the Income Statement until a transaction is ‘earned and substantially complete.’

As a result, we defer recognition of the Sale and move the Revenue to the Company’s Balance Sheet as a Liability account until the Company ‘earns’ the underlying Revenue.

We then recognize Revenue and wind the Liability down when the Company delivers the good or service to the Customer.

Want To Learn More About Finance?

Check out all of our (free) deep-dive articles in our Analyst Starter Kit:

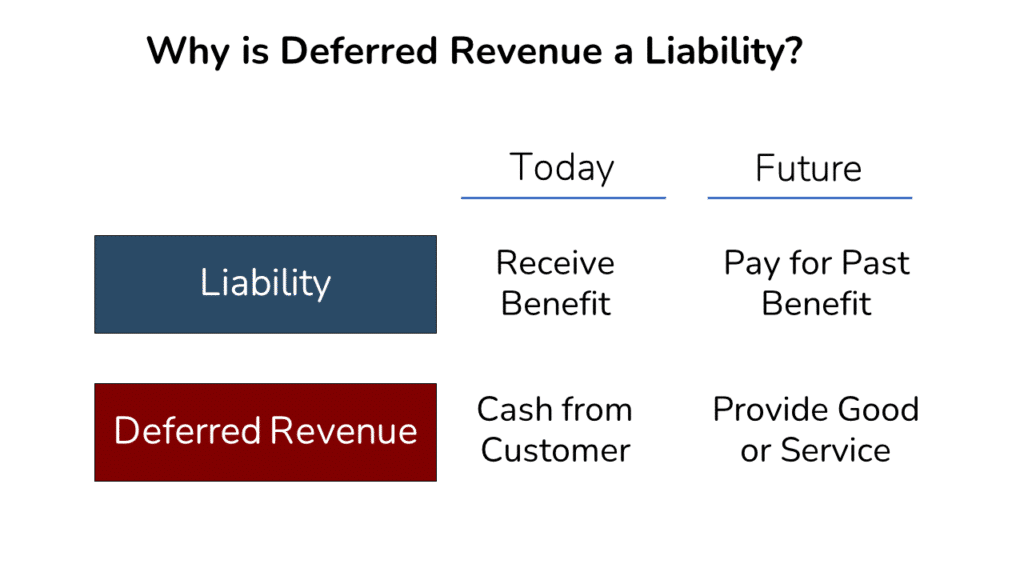

Why Is The Deferred Revenue Account a Balance Sheet Liability?

A common question that comes about at this point is, ‘Why do we record Deferred Revenue as a Liability? It seems more logical that we would reflect it as an Asset Account.‘

To answer that question, we should revisit the fundamental substance of a Liability.

With any Liability, we receive a benefit today but owe payment in the future.

With Deferred Revenue, the Company receives a benefit (i.e. Cash) now from the Customer prepayment.

However, the Company owes delivery of the goods or services to the Customer in the future.

Because delivery of the future goods or services owed is the responsibility of the Business, we record a Liability.

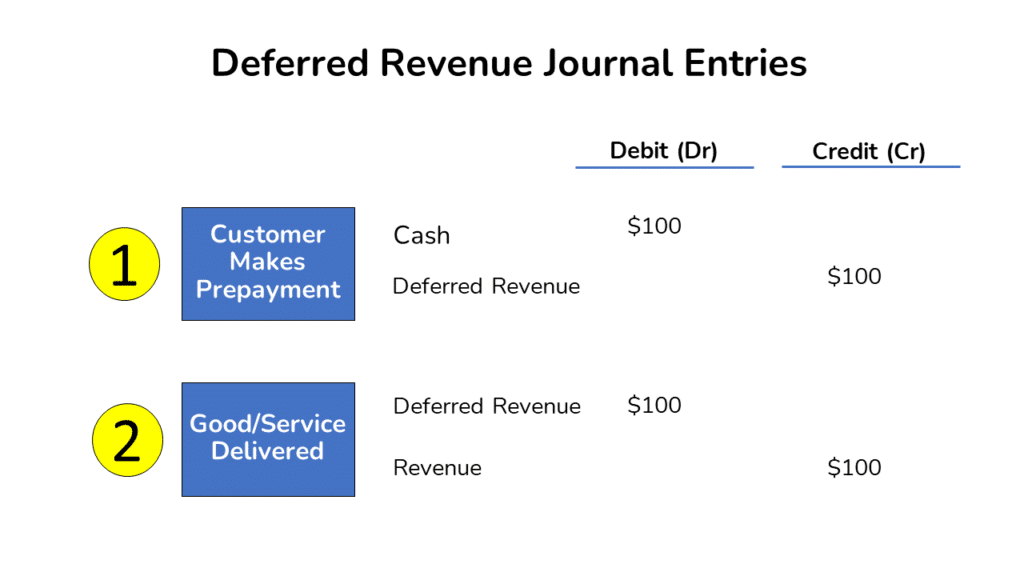

Now let’s take a look at how we would record the above transactions in terms of Debits and Credits.

Deferred Revenue Journal Entry

In Accounting, we record transactions as Journal Entries with Debits and Credits.

Below we walk through the two typical Journal entries for Deferred Revenue.

How to Record Deferred Revenue Journal Entries

- Customer Makes Prepayment for Future Delivery of Good or Service

Debit Cash to reflect the inflow of Cash to the Business.

Credit Deferred Revenue to reflect the fact that the Company now owes the customer a Good or Service in the future. - Good or Service is Delivered/Earned

When the good or service is delivered to the customer, we Debit the previously recorded Liability to reflect the fact that the prior obligation has been satisfied.

And we Credit Revenue to reflect that the Good or Service has been delivered and that the transaction is now earned and substantially complete.

Now let’s switch gears and look at a real-life example of Deferred Revenue.

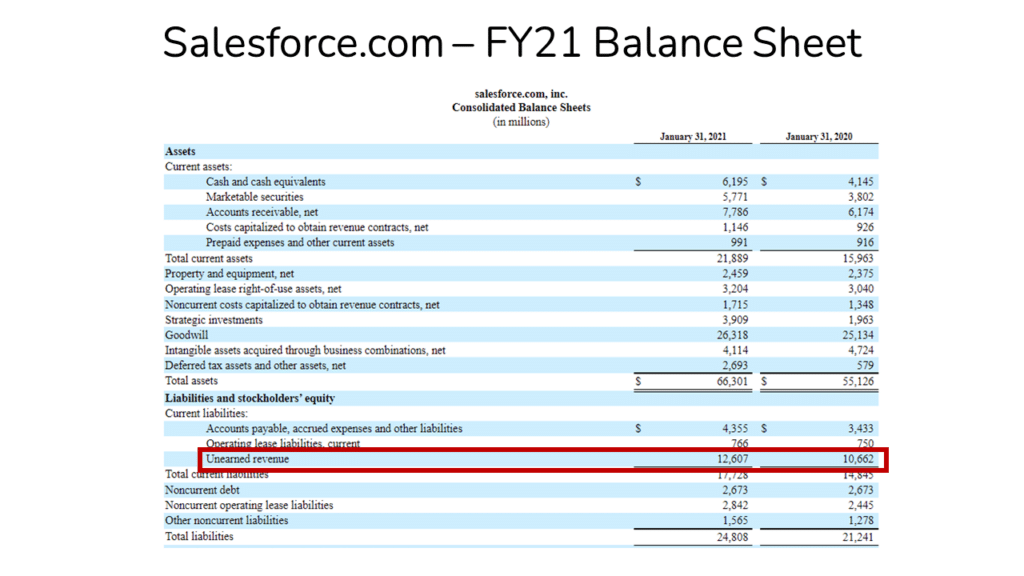

Example of Deferred Revenue: Salesforce.com

In real life, Software as a Service (SAAS) Businesses typically have significant Deferred Revenue.

In this example, we’ll look at Salesforce.com, one of the largest Customer Relationship Management (or ‘CRM’) SAAS businesses.

The high level of Deferred Revenue arises because SAAS businesses typically offer customers significant discounts in return for paying in advance for their services.

We can find the total balance of Salesforce.com’s Deferred Revenue on the Company’s Balance Sheet.

In Salesforce’s Balance Sheet, we can see that the Company has received nearly $13 billion in Customer Prepayments for which it owes future services.

It’s important to capture the fact that this large Deferred Revenue balance will have zero impact on the Income Statement (Revenue –> Net Income) until Salesforce delivers the underlying products and services to Customers.

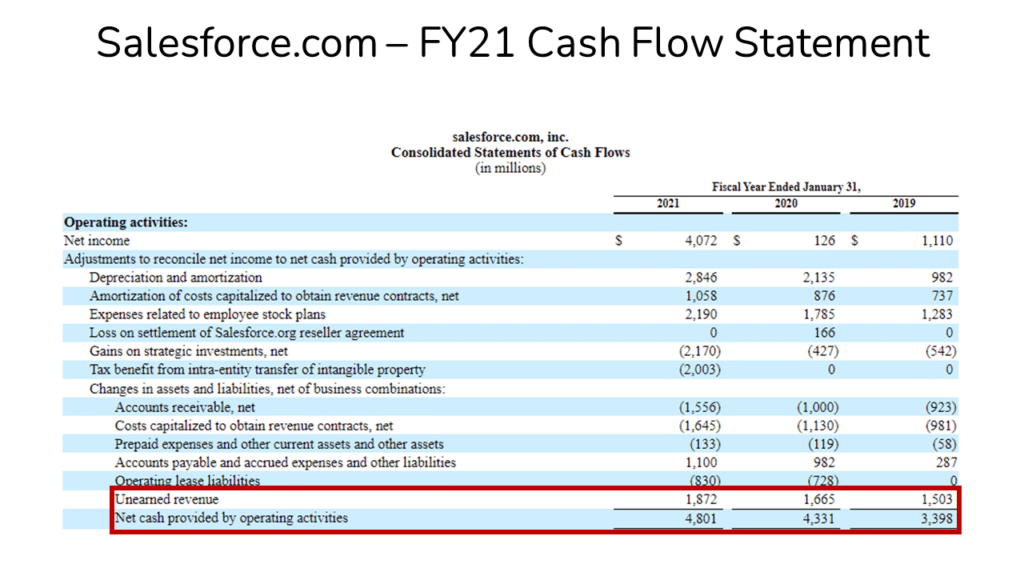

If we switch over to the Cash Flow Statement, we can see that Unearned Revenue (i.e. ‘Deferred Revenue’ or ‘Unearned Income’) has created $1.5-1.9 billion of annual incremental Cash Flow for Salesforce year in the last three years.

Said differently, ~40-45% of the Company’s Cash Flow from Operations has come from Deferred Revenue!

As you can see, Deferred Revenue provides a major benefit to Salesforce.com’s business by generating significant excess Cash Flow.

However, as we said earlier, Salesforce now owes those services to customers in the future.

Now that we’ve looked at a real-life example with Saleseforce.com, let’s now answer a few common questions that pop up related to Deferred Revenue.

Wrap-Up: Deferred Revenue

![An image of a stick figure sitting at a desk understanding [keyword]](https://cdn-cakli.nitrocdn.com/tPWroFPPCbHctVuRmyRSUFBgFveYsqEw/assets/images/optimized/rev-d28a71c/finance-able.com/wp-content/uploads/2021/11/stick-figure-understanding-deferred-revenue-1024x576.png)

Hopefully, you now have a much better understanding of the ins and outs of Deferred Revenue.

Let us know if you have any questions in the comments below.

You can also send comments, feedback, or suggestions for new article topics to admin@finance-able.com.

We’d love to hear from you!

About the Author

Mike Kimpel is the Founder and CEO of Finance|able, a next-generation Finance Career Training platform. Mike has worked in Investment Banking, Private Equity, Hedge Fund, and Mutual Fund roles during his career.

He is an Adjunct Professor in Columbia Business School’s Value Investing Program and leads the Finance track at Access Distributed, a non-profit that creates access to top-tier Finance jobs for students at non-target schools from underrepresented backgrounds.

Frequently Asked Questions

Deferred Revenue is created when a customer prepays for a future good or service. Because we only record Revenue when its earned and substantially complete, we initially record Deferred Revenue as a Liability (reflecting the value of the good or service to be delivered).

When the business delivers the good or service to the Customer, we eliminate the original Liability and record Revenue.

We record Deferred Revenue as a Liability upon prepayment by the Customer.

When the business delivers the good or service owed to the customer, we then record Revenue and simultaneously eliminate the original Liability that we created at the time of the Customer prepayment.

Deferred Revenue reflects an obligation to deliver goods or services to a Customer in the future. As a result, Deferred Revenue is recorded as a Liability.