Master the concept of Negative Working Capital so you can use it on the job in Investment Banking, Private Equity, and Investment Management.

In this article, you will learn:

- Why Negative Working Capital matters.

- How Negative Working Capital creates excess Cash Flow (essentially a ‘Free Loan’) for a Business.

- The two primary drivers of Negative Working Capital.

- How Amazon used Negative Working Capital to raise $10 million in funding before its IPO.

Estimated reading time: 14 minutes

TL;DR

- Negative Working Capital results when Current Liabilities exceed Current Assets.

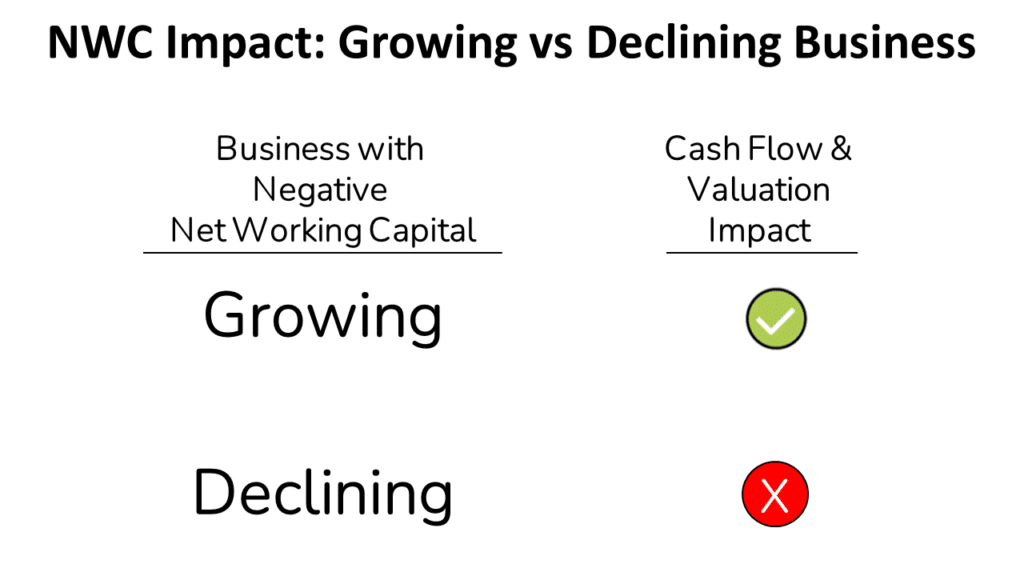

- A Negative Working Capital situation creates excess cash for a growing business but requires cash investment as a business declines.

- Negative Working Capital drives incremental cash flow and thus a higher valuation for a perpetually growing business.

Want To Learn More About Finance?

Check out all of our (free) deep-dive articles in our Analyst Starter Kit:

Why Does Negative Working Capital Matter?

Negative Working Capital is a critical concept to master if you are aiming for (or working in) Finance.

The concept of Negative Working Capital is often not well understood as a bit of a confusing concept. In this article, we will provide a variety of illustrations to make the concept clear.

Let’s start with what is Negative Working Capital and how is it created?

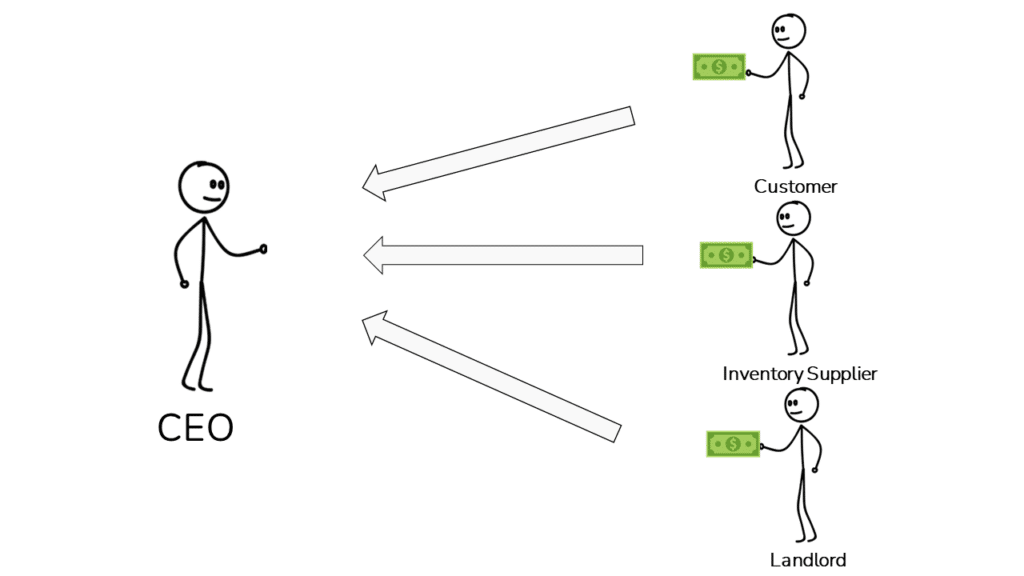

First, Negative Working Capital arises when Current Liabilities exceed Current Assets.

This dynamic arises when operating lenders (e.g., inventory suppliers, landlords, and customers) provide funding greater than what is required to fund items like Accounts Receivable and Inventory.

Typical Sources of Negative NWC

Excess funding from Operating Lenders might sound great at first glance.

But, as we will see, Negative Working Capital can cause significant problems when a business declines.

Now let’s look at how the Negative Working Capital concept shows up in Interviews.

Negative Working Capital in Interviews

The topic of Negative Working Capital may arise in finance interviews.

However, it is not nearly as common as other technical finance interview questions like ‘Walk Me Through a DCF’ or ‘Walk Me Through an LBO.’

A few common interview questions on the topic are:

- What is the Working Capital Formula?

- How do you Calculate Working Capital?

- What is Negative Working Capital?

- Is Negative Working Capital bad?

- How does Negative Working Capital impact Cash Flow and Valuation?

To answer these questions, you will need to understand:

- The technical meaning of Negative Working Capital (covered below).

- The Cash Flow and Valuation impacts of Negative Net Working Capital (go to section).

After reading this article, you will nail all of the Interview Questions above.

Let’s dive in!

What is Working Capital?

Let’s kick off our discussion here with a quick refresher on the concept of Working Capital.

We can view Working Capital through a few different lenses. We’ll explore two of the most common here:

- The Accounting Definition of Working Capital.

- The Business Owner view of Working Capital.

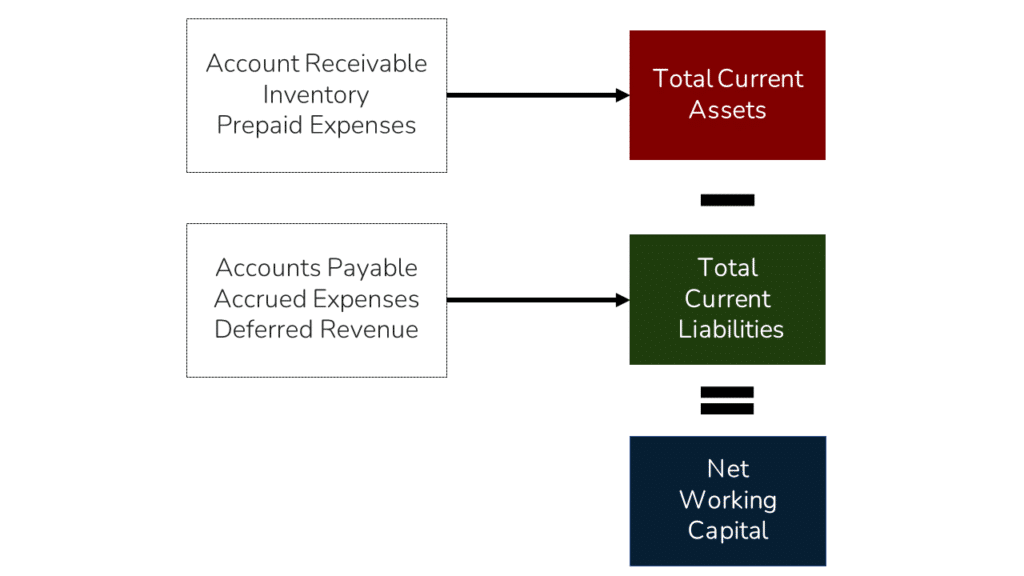

The Accounting Definition of Working Capital

The most basic definition of Working Capital is the Accounting definition that most people learn early in their Finance learning journey.

The calculation for Working Capital is Current Assets minus Current Liabilities.

Note: Current Assets in the definition above excludes cash.

This formula essentially captures a Business’ investment in short-term Operating Assets and the degree to which the Assets cover the short-term obligations of the Business.

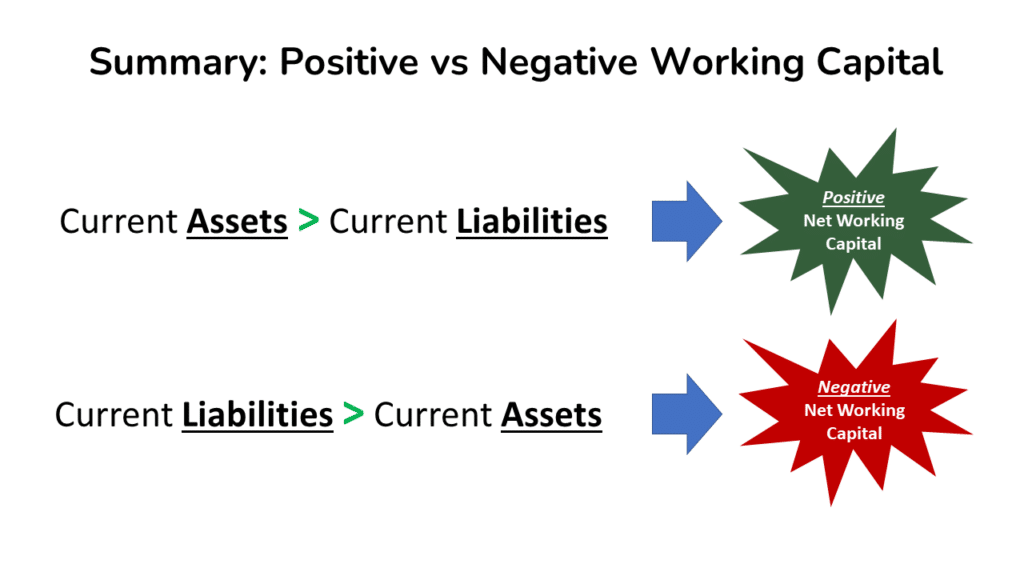

Positive vs Negative Working Capital

From the Working Capital formula above, we can see that Working Capital can have one of two potential states:

- Positive Working Capital: Current Assets > Current Liabilities

- Negative Working Capital: Current Liabilities > Current Assets

To begin with, the vast majority of Businesses have Positive Working Capital.

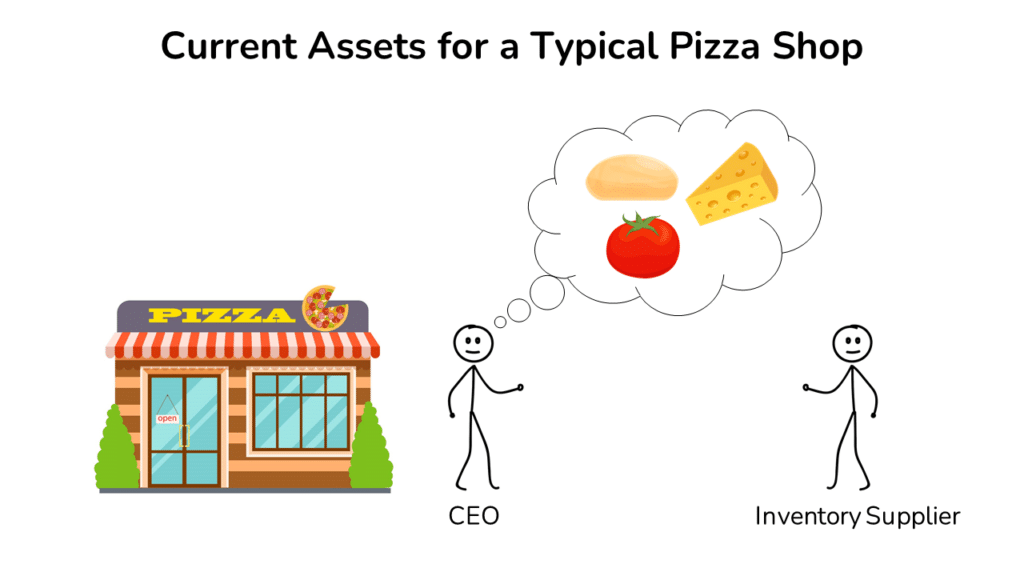

For example, the working capital requirements of a restaurant like a Pizza Shop in most cases would result in Positive Working Capital.

With a Pizza Shop, the owner’s current Assets would primarily consist of Inventory (flour, sauce, cheese, etc.).

The Inventory suppliers are unlikely to extend overly generous payment terms to the Pizza Shop.

So the Pizza Shop’s Current Assets will generally exceed Current Liabilities.

However, as we’ll see shortly, some businesses have ways of getting suppliers and customers to lend beyond the level of Current Asset funding needs.

Now that we have clarified fundamental Working Capital definitions let’s switch gears to how Business owners view Working Capital.

The Business Owner’s View of Working Capital

From an owner’s perspective, the Working Capital of a Company is more likely to be viewed as ‘Trapped Cash.’

In other words, Working Capital reflects the cash tied up in the Business.

To explain further, as Current Assets increase, they require funding.

Said differently, an increasing Asset is a ‘Use of Cash.’

On the other hand, as Current Liabilities increase, they offset the funding required.

As such, an increasing Liability is a ‘Source of Cash.’

As a Business Operator, wouldn’t you prefer to have fewer ‘Uses of Cash’ and more ‘Sources of Cash?’

We will dive deeper into that question in the coming sections.

The Two Drivers of Negative Working Capital

Earlier in the article, we said that some businesses have Negative Working Capital.

Again, to have Negative Working Capital, a Business’ Current Liabilities must exceed Current Assets.

But how do we get someone to lend us more than the value of our Assets?

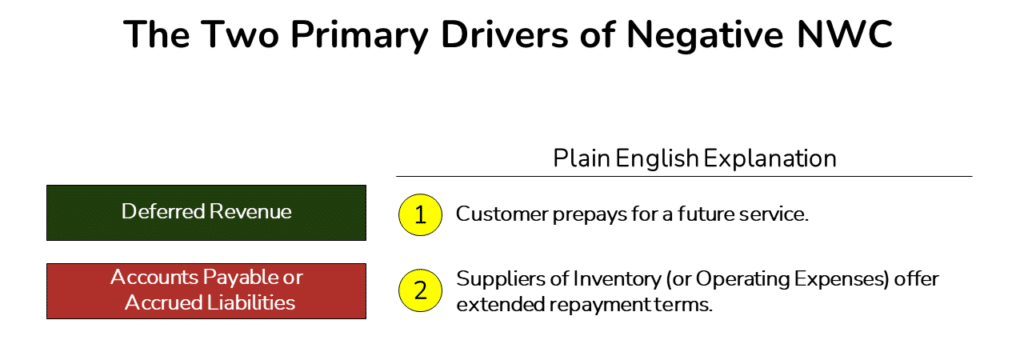

The answer is that there are two primary drivers of Net Working Capital:

- Customer prepayments (i.e.,Deferred Revenue).

- Delayed payment on Operating Liabilities.

In the next section, we’ll explore each of these drivers in detail.

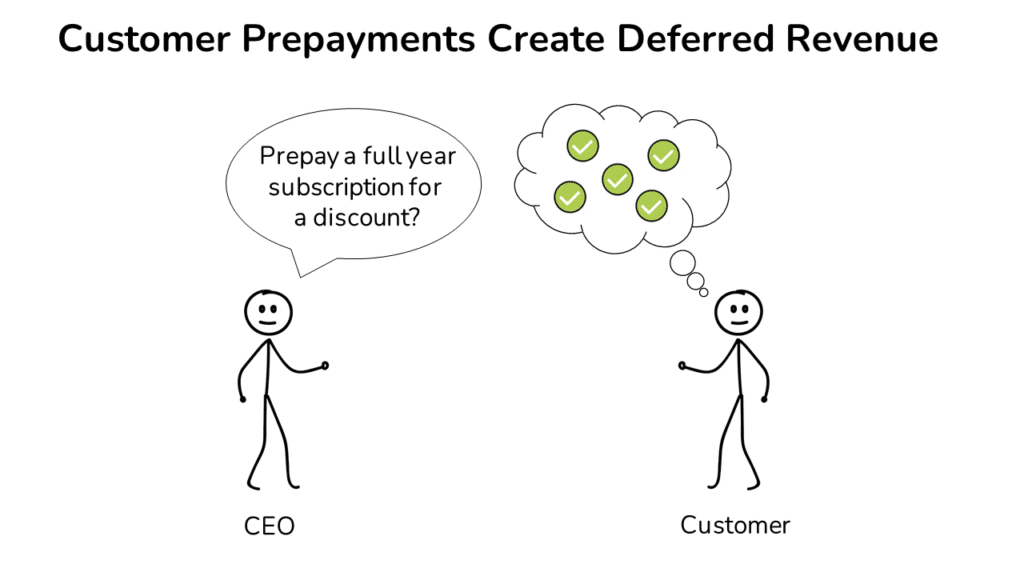

Negative NWC Driver #1: Deferred Revenue

Let’s begin with customer prepayments which we formally call ‘Deferred Revenue.’

The best example of Deferred Revenue is a subscription business where a customer pre-pays for a year-long subscription for a service like Apple Music.

When a customer pre-pays for a subscription (typically in exchange for a discount), the Business receives the cash up-front. We record this transaction as a Current Liability called Deferred Revenue.

We record Deferred Revenue as a Liability because the Business now owes the customer a service in the future.

In the meantime, the Business benefits from a cash inflow that is essentially a free loan until the customer receives the service.

Deferred Revenue is a core driver of Negative NWC for all sorts of subscription-related services from Apple Music to Salesforce.com.

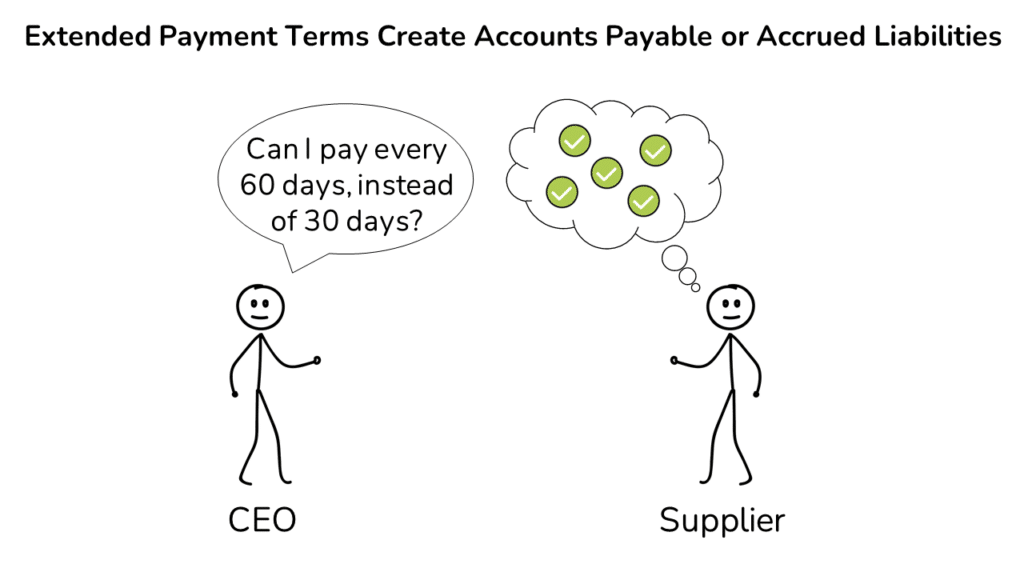

Negative NWC Driver #2: Accounts Payable + Accrued Liabilities

The other core driver of Negative Working Capital is favorable payment terms from operating suppliers, including:

- Accounts Payable: money lent by Inventory suppliers.

- Accrued Liabilities: money lent by other operating suppliers (landlords, utility providers, etc.).

Overly generous payment terms typically only come about when the Business has significant leverage over a supplier.

Now let’s look at a more tangible example of how a company benefits from extended payment terms.

Example: Accounts Payable Creating Negative Working Capital

Step 1: An Inventory supplier allows a Business to pay for their Inventory 60 days after they purchase it (as opposed to 30 days).

Step 2: The Business cycles through (i.e., sells out of) that Inventory in 30 days.

Step 3: The Business now has the cash needed to repay the money owed for the Inventory by Day 30.

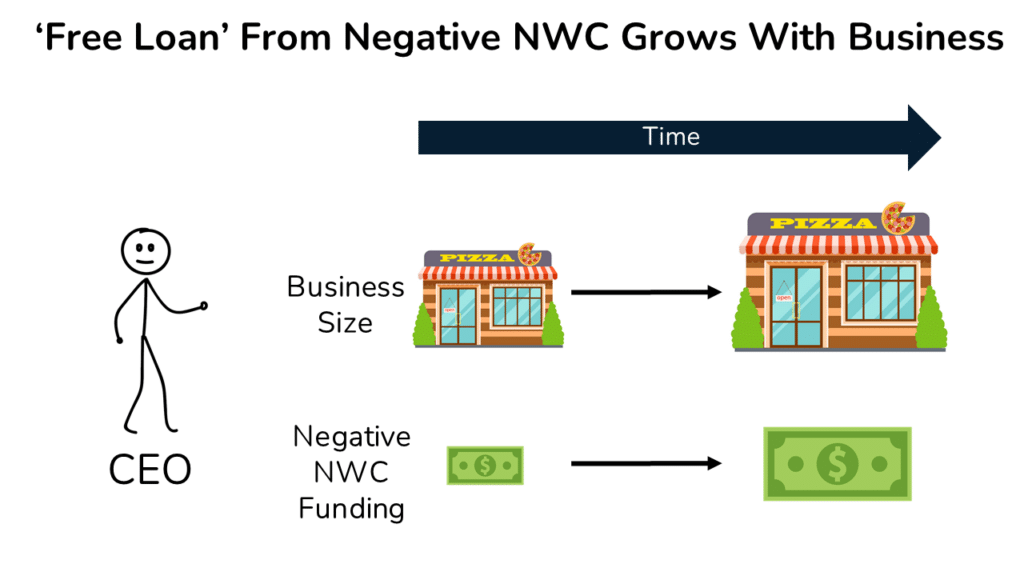

30 Day Customer Collections vs 60 Day Payment

So, for days 31-60, the Inventory Supplier essentially provides a ‘free loan’ to the Business!

And, assuming the Negative Working Capital grows in line with the growth of the Business, the dollar value of the ‘free loan’ will grow over time!

Now that we understand the underlying drivers of Negative Working Capital, we’ll dive into how Negative NWC impacts Cash flow and Valuation.

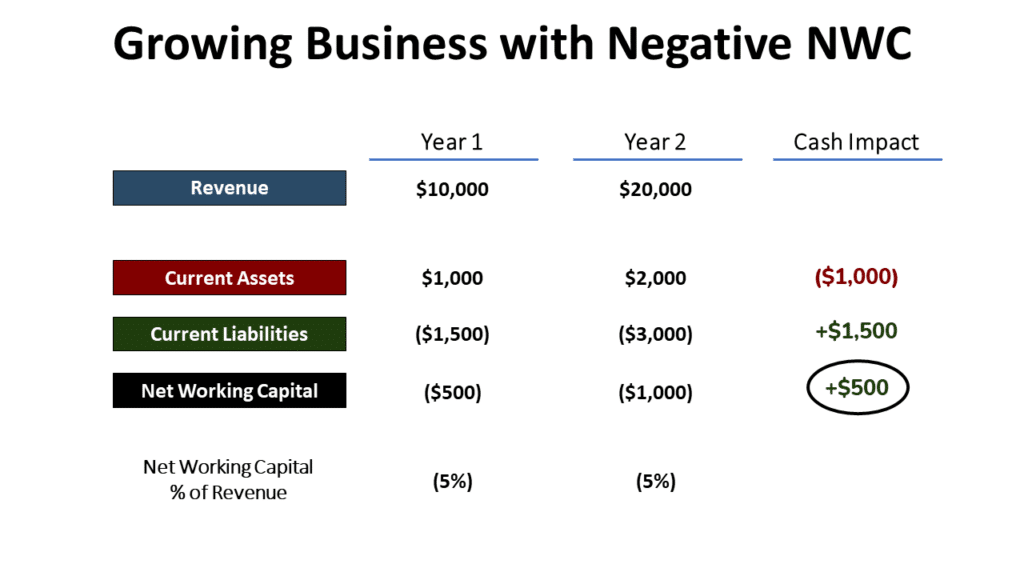

Impact of Negative NWC on Cash Flow

Following what we said in the section above, as a Business grows in size, the dollar value of the short-term funding from Negative NWC grows in tandem.

Said differently, each year, the dollars required to fund increasing assets are lower than the dollar value from increased funding from money lent from Customers, Inventory Suppliers, and Operating Suppliers.

Assuming Negative NWC remains proportional to Revenue, this results in recurring excess cash inflows to the Business.

For a deeper dive into these mechanics, check out our illustrated deep-dive videos here:

Impact of Negative Working Capital on Valuation

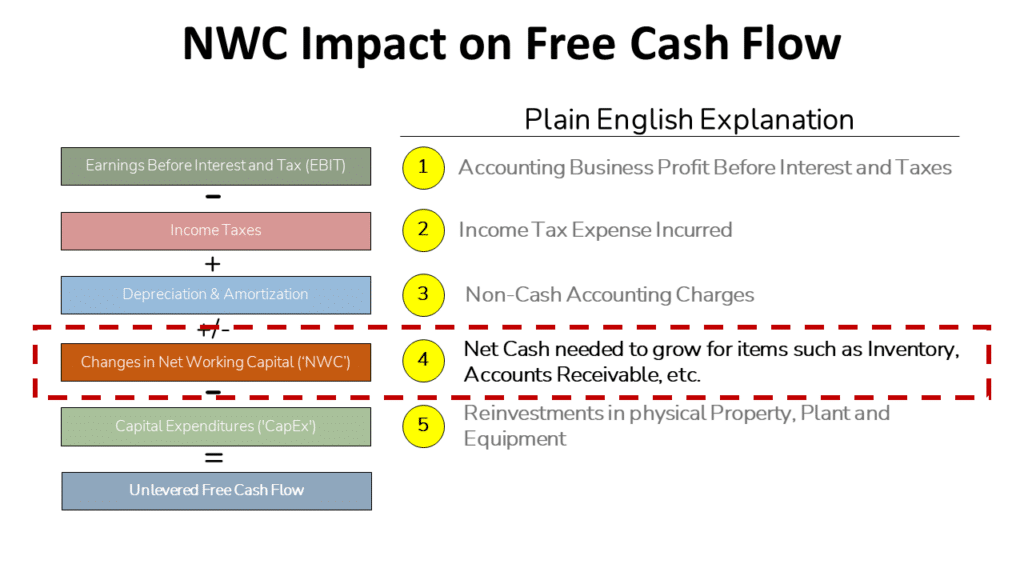

In our Walk Me Through a DCF article, we explained why Cash Flow is the underlying driver of the Valuation of a Business.

In the diagram below, from our DCF article, you can see that the change in Net Working Capital is a core driver of the Cash Flow used to value a business.

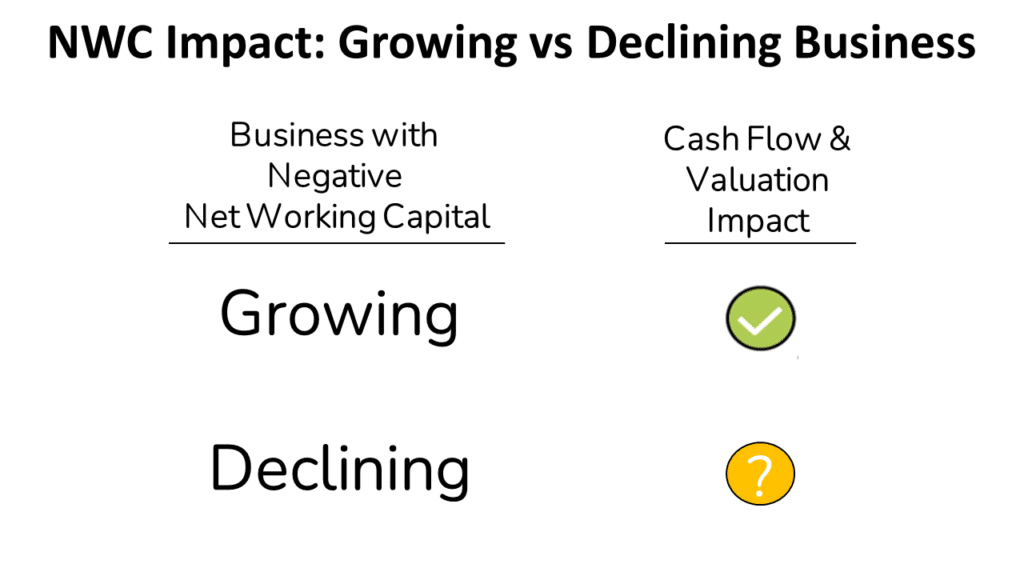

In the last section, we said that Negative NWC creates recurring extra cash inflows as a Business grows.

So, if a business with Negative NWC grows into perpetuity, its Valuation will be higher than a business with Positive Working Capital.

To tie the last two sections together, the advantages of Negative Working Capital are:

- Recurring Excess Cash Flows

- Higher Valuation

Sounds like Business nirvana, doesn’t it?

The catch is…that most businesses don’t grow forever!

When Negative Working Capital Goes Wrong

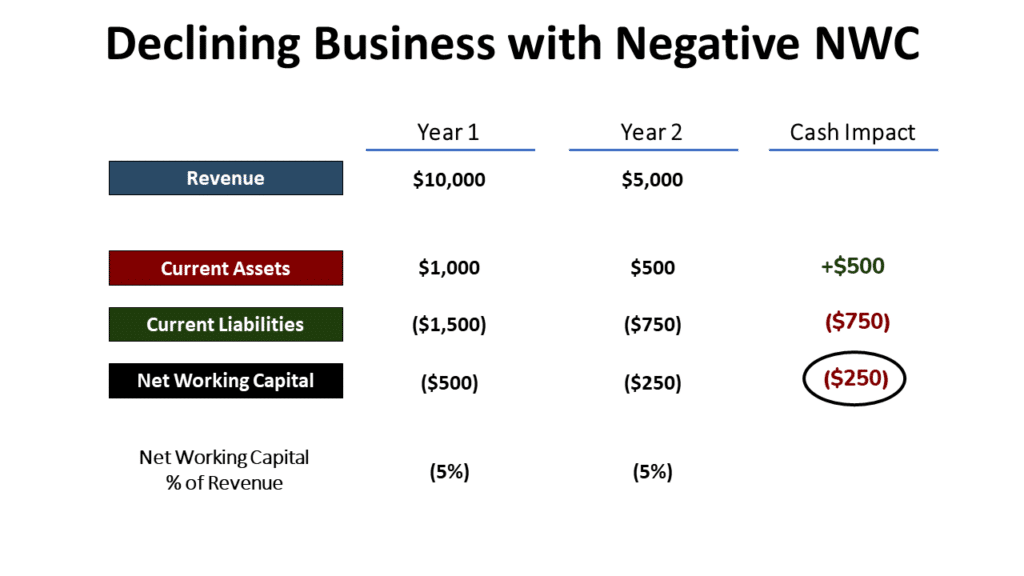

When a business with Negative NWC declines, it experiences MAJOR issues.

In addition to the typical challenges that occur when a business declines (less profit, instability, etc.), the Business requires cash funding on the way down.

To keep this simple, in the example below, we’ll assume that all the components of Working Capital decline in proportion to Revenue.

The cash funding need arises because the dollar value of Current Liabilities that come due exceeds the cash inflows from the declining Current Assets.

So, in the end, Negative NWC is a double-edged sword. It’s fantastic on the way up and terrible on the way down!

Now let’s look at a real-life example of Negative Working Capital in action with Amazon.com.

Negative Working Capital Example: Amazon

Since its founding, Amazon.com has maintained a Negative NWC balance.

Negative Working Capital has provided Amazon essentially free funding that currently sits at $67 billion (Source: sec.gov) as of June 30, 2021.

What is less well appreciated is the role Negative NWC played in Amazon’s early years.

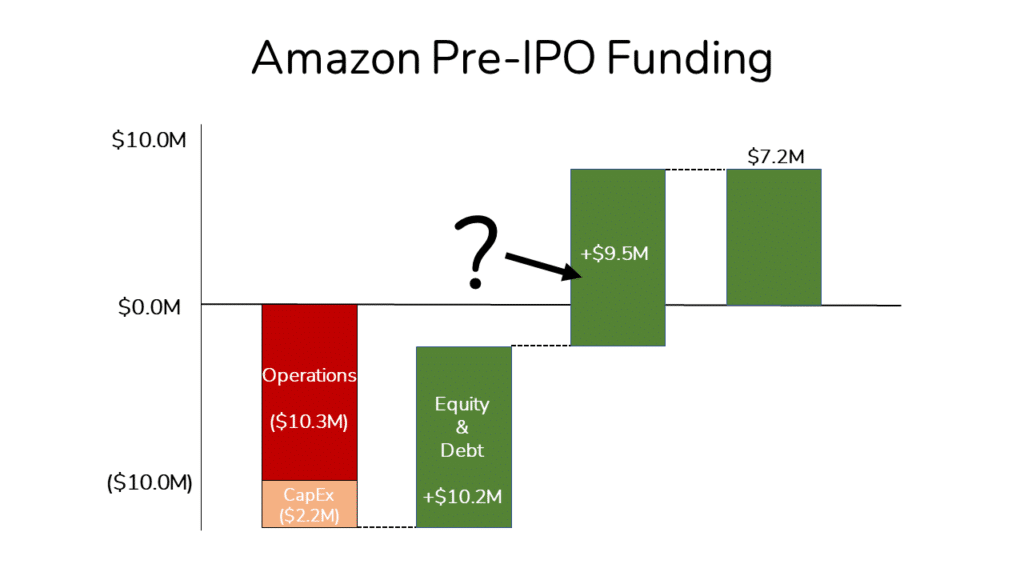

Before Amazon’s Initial Public Offering (IPO), the Company raised $10.2 million in funding, with the majority coming from venture capital funding.

Here’s the thing, it cost ($12.5) million to run Amazon from start-up through the quarter leading up to the IPO.

So Amazon should have been short on cash by ($2.3) million, right?

Wrong! Amazon’s cash balance stood at $7.2 million at end of the quarter just prior to its IPO!

Source: sec.gov

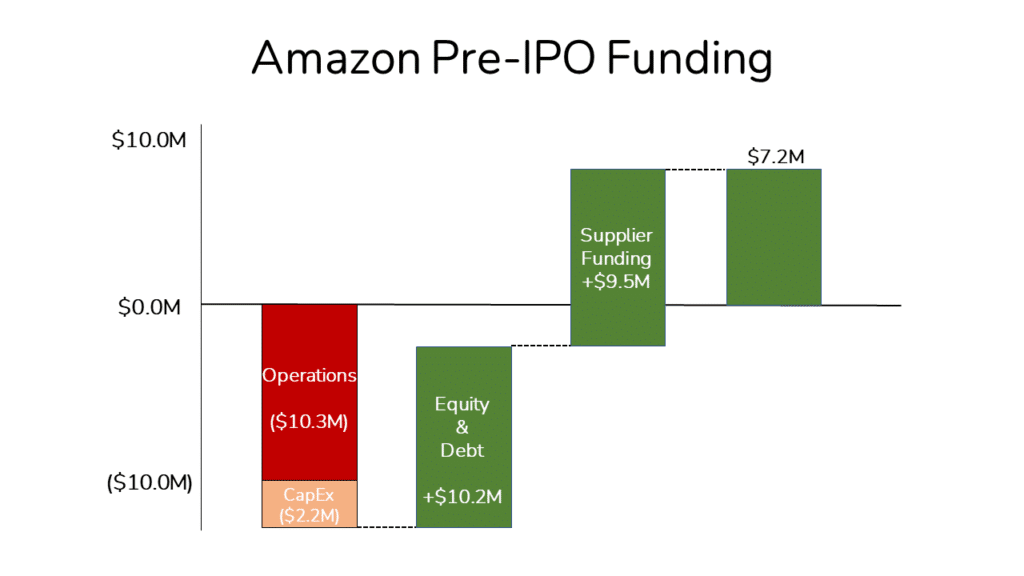

So, where did the other $9.5 million in Cash come from?

Answer: Amazon’s Pre-IPO Funding

The answer is that Amazon relied heavily on supplier financing (i.e. Negative Working Capital) to fund their operations in these earlier years.

The Company raised nearly $10 million of essentially interest-free funding from Suppliers via Negative Working Capital.

Source: sec.gov

In short, if Amazon had not had Negative NWC, it would have been required to raise nearly $10 million of additional capital, resulting in far lower ownership for the founding shareholders.

Wrap-Up: Negative Working Capital

Hopefully, you now have a much better understanding of the underlying idea and the ultimate Cash Flow and Valuation impacts of Negative Working Capital.

Negative Working Capital is important because it can have a material impact on a company’s Cash Flow (and thus its Valuation).

Let us know if you have any questions in the comments below. We’d love to hear from you!

About the Author

Mike Kimpel is the Founder and CEO of Finance|able, a next-generation Finance Career Training platform. Mike has worked in Investment Banking, Private Equity, Hedge Fund, and Mutual Fund roles during his career.

He is an Adjunct Professor in Columbia Business School’s Value Investing Program and leads the Finance track at Access Distributed, a non-profit that creates access to top-tier Finance jobs for students at non-target schools from underrepresented backgrounds.

Frequently Asked Questions

Negative Working Capital can be good or bad, depending on the trajectory of the Business. For example, if a business is growing, Negative Working Capital can create extra cash flow. However, a Business with Negative Working Capital declines, it will likely require funding on the way down, which is often problematic.

Negative Working Capital is a double-edged sword. It’s excellent for growing Businesses (greater Cash Flow and often Valuation) but terrible for declining Businesses (requires cash investment during decline).