Learn How to Value a Business with a simplified, Plain English explanation that uses the House you live in as an Analog. We’ll cover everything from the basics to more advanced business valuation methods like Discounted Cash Flow Analysis.

Estimated reading time: 12 minutes

TL;DR

- Learning How to Value a Business is central to nearly any role in the Finance world.

- The two most common Business Valuation Methods are Intrinsic (Cash Flow-Based) Valuation and Multiple-Based Valuation.

- The basis for valuing the vast majority of Businesses is their future Cash Flows.

- To value future Cash Flows, we perform a Discounted Cash Flow (DCF) analysis which utilizes Discounting to pull future Cash Flows back to today.

- The total value of all future Cash Flows when Discounted back to today gives us the Purchase Price of the Business (or Enterprise Value).

Want To Learn More About Finance?

Check out all of our (free) deep-dive articles in our Analyst Starter Kit:

Introduction – How to Value a Business

Welcome to Article #2 in our Learn Finance ASAP series!

In this article, we’ll dig into the concept of Intrinsic (i.e. Cash Flow-Based) Valuation and how it applies to both Houses and Businesses.

If you missed our first article in the series, we recommend that you read it before diving into this one.

In that article, we explained that both Houses and Businesses are Cash Flow Generating Assets (or CFGAs for short).

In this article, we’ll add to our Mental Model by showing that any CFGA (including Houses and Businesses) is valued based on the future Cash Flows that they generate.

But we need to quickly tackle one thing first!

In my experience, training on Business Valuation Methods often fails to include an overview of when and why we are valuing things in the first place.

That’s where we’ll start to give you a big-picture view of a few real-life scenarios where Finance Professionals utilize the Business Valuation Methods we’re about to explore.

Once we’ve nailed down the when and why, we can get into the nuts and bolts of this and further add to the Mental Model we started building in Article #1.

Why Do We Need To Value a Business? Who Really Cares?

In Article #1, we said that a core question in Finance is, “What is the business worth?”.

Let’s take a look at a few examples of where that question might arise:

- Investment Banking: A client hires you to sell their business and you need to figure out how much they should sell it for.

- Private Equity: Your team decides to buy a company and you need to work out its value to know how much you should pay for it.

- Investment Management: A portfolio manager asks you how much the value of a stock could increase over the next year and you need to determine its projected valuation.

- Corporate M&A: You want to make an acquisition but you’re not sure if the price proposed by the seller makes sense.

To answer any of these questions, we need a strong understanding of Business Valuation.

How to Value a Business: Two Common Methods

Broadly speaking, there are two major Business Valuation Methods: Intrinsic Valuation and Multiple-based Valuation:

- Intrinsic Valuation: we value the Business (or House) based on the Cash Flows that it will generate in the future.

- Multiple-Based Valuation: we look at the Purchase Price of a Business relative to its Cash Flow.

As we’ll see in Article #3 in this series, Multiple-Based valuation is just a ‘shorthand’ method. In fact, it’s actually an Intrinsic Valuation in disguise. More on that later.

For now, we’re going to focus on the Intrinsic Valuation methods.

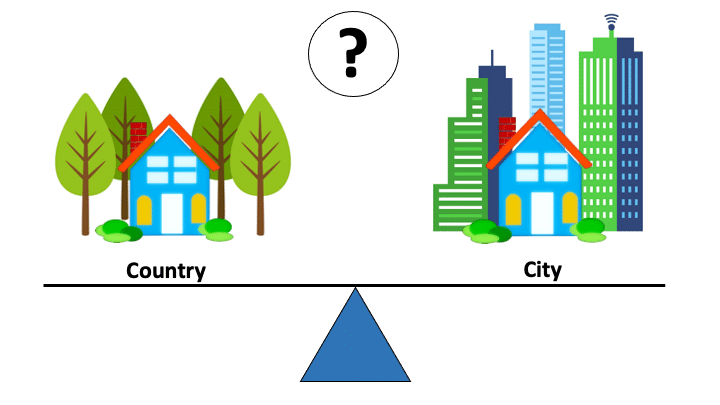

How to Value a Business: House Example

Let’s imagine (as we did in Article #1) that we rent out our House and, as such, that it becomes a ‘Business‘.

In this situation, though, we’ll add a twist and change the example to two Houses that we own and rent out:

- House #1: Located in a remote, rural area.

- House #2: Located in a big city (e.g. San Francisco, New York, etc.).

Let’s also imagine that both Houses are:

- The same exact size.

- Sit on land that is the exact same size.

- Are built with the exact same materials.

Based on the information above, if you were to sell each house tomorrow, which would be worth more?

The Answer

Was your answer the house in the City?

It seems like intuitive that it would be the case, right?

Well, you are correct. But why is that the case?

Weren’t the houses both the same size?

Didn’t they sit on the same sized plot of land?

Weren’t they build with the exact same materials?

The reason one is worth more than the other is Cash Flow!

Despite their many similarities, the fact that you can charge FAR more to rent out a house in a Major City (in most cases) than in a Rural area makes the city house worth more.

In short, the amount of rental income you could generate (i.e. Cash Flow) from a house is what drives what buyers will pay.

Even if, as buyers, we don’t usually look at houses as potential businesses or think about a house this way when we purchase a House.

Note that in this instance, we’re assuming the cost of building both physical houses (or Asset Value) is the same. This is a bit of a simplifying assumption, but it helps us to build out our Mental Model for now…so let’s stick with it.

In short, Asset Value is not relevant to each House’s worth, since the Cash Flow value is greater.

The punchline is that a House is a Cash-Flow Generating Asset and the value for CFGA’s is a function of their future Cash Flow generation potential.

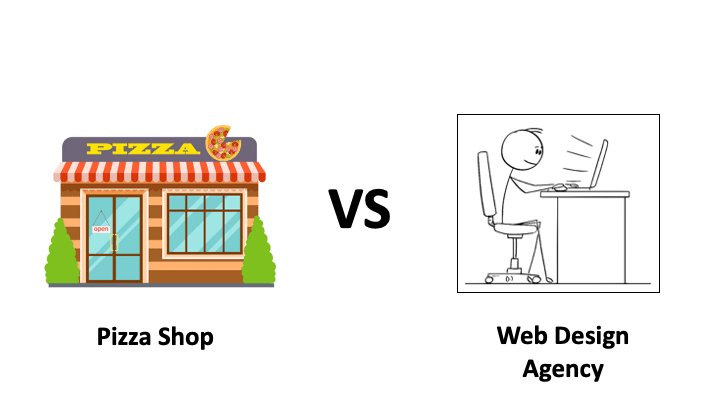

How to Value a “Traditional” Business

If we switch our example to a traditional Business, we find that the same applies.

Let’s look at two different types of businesses:

- A Goods Business: Pizza Shop.

- A Service Business: Freelance Web Design Agency.

These examples will illustrate how Intrinsic Valuation functions exactly the same way for a Business as it does for a House.

Business Valuation #1: Pizza Shop

If we decided to start a pizza shop tomorrow, we’d look to buy (or more likely Rent) a store.

Once we find our store, we’d also need to buy a bunch of additional items.

For example, we would need ingredients for our Pizza, a few Ovens, and numerous other items to ensure the Pizza Shop can operate effectively.

Let’s assume that all of this costs us $200,000.

Let’s say that our pizza shop is a MAJOR success and people can’t get enough of our pizza. In our first year, we generate a cash profit of $400,000.

Now, let’s fast forward to the end of year one.

Someone approaches you and offers to pay $200,000 for the Business since that’s what you initially paid for it (i.e. the Asset Value).

Would you take the offer?

Nope! You’d probably laugh them out of your store and go back to selling pizza. 😊

Hold that thought and let’s take a look at our next business.

Business Valuation #2: Freelance Consulting

Now, let’s imagine that you start a Freelance Web Design Agency. You hire 10 people to help you with the workload.

For this, you’ll need to buy Computers for all of your employees and any necessary software for web design.

Let’s assume that all of this costs you $50,000.

As was the case with the Pizza Shop, let’s imagine that your Business takes off like a rocket!

You make $200,000 in one year and see even more potential to grow going forward.

Again, someone approaches you to buy the business. They offer $50,000 since that’s what you paid to start the Business.

Would you sell the business for the same $50,000 you paid to initially get the business started? Again, clearly not!

How to Value a Business: Asset vs Cash Flow

In both cases above (as well as with our Houses), the future Cash Flow value far exceeds the Asset Value, and we’ll generally defer to the higher of the two for Houses, Businesses, and any Cash Flow Generating Asset!

Generally speaking, compiling a group of assets to generate a far greater cash flow than their original value is the primary objective when starting a Business.

As we can see above, Asset Value tells us what we paid in the past, but Cash Flow Value tells us about the value the business will create in the future.

In short, Cash Flow Value is the underlying driver behind nearly all Business Valuation.

Awesome… So, How Do I Value Future Cash Flows?

The next natural question you might be asking is…How do we actually value Cash Flows?

Especially since they both occur in the future and are unpredictable.

To value Cash Flows, we only need two tools:

- Tool #1: Discounting (aka Time Value of Money).

- Tool #2: Discounted Cash Flow Analysis (aka DCF Analysis).

Let’s take a look at each of these tools in action!

Business Valuation Tool #1: Discounting

To begin with, we said that the Valuation of a House or a Business is a function of Cash Flows.

The issue is that those Cash Flows…exist in the future.

And we need to value those Cash Flows as of today.

Discounting is what allows us to make this happen.

The short story with Discounting is that if we receive cash Today (as opposed to in the Future), we can generate a return on that money in the meantime.

As a result, there is a cost to receiving money in the future vs today (a concept formally called the Time Value of Money) because you lose the opportunity to generate a return on that money.

As we go further and further into the Future, the cost increases. That’s because we’re missing out on more and more of a return that could have been generated (an Opportunity Cost in finance-speak).

Discounting is a process that adjusts future cash flows to reflect this cost, which basically brings the Future dollars back to today and allows us to value the Future cash flows as if we received them Today.

Don’t worry so much about the Math in the image below for now. In short, we use Discounting to pull Future dollars from the future back to Today.

Business Valuation Tool #2: Discounted Cash Flow Analysis

In a Discounted Cash Flow analysis, we make detailed projections of our Cash Flows until the business achieves a Steady-State Growth Rate that equals the level of growth of the overall economy. This usually takes us 5-10 years into the future for most businesses.

Beyond that point, we have a few other tools to estimate the projected Cash Flows for all other future years. We explore these tools in detail in our Finance|able Valuation course (Coming Soon!).

Once we have our projections laid out, we use the Discounting tool discussed above to bring the Cash Flows back to today.

When we pull all the future Cash Flows of a House or Business back using Discounting, we will end up with a single dollar value.

This single dollar value is the price we would pay for the right to receive all of those cash flows in the future.

That single dollar value is what we would pay for the business today… or the Valuation of the Business (or House).

In the Finance world, we need fancy terms for everything; so instead of calling this value Purchase Price, as you would for a House, we call it Enterprise Value when discussing Business Valuation.

Wrap-Up: How to Value a Business

In short, the price we pay for any House or Business is basically what we would pay for the right to all the future Cash Flows of the House or Business…or any Cash Flow Generating Asset for that matter.

To calculate this value, we would construct a Discounted Cash Flow Analysis which uses Discounting to value Future Cash Flows as of Today.

Now, let’s have a quick look at a few final points.

First, let’s recap the components of our Mental Model that we’ve built thus far:

- A House and a Business are both Cash Flow Generating Assets (CFGA’s)and share the same characteristics.

- The underlying driver of the Intrinsic Valuation for nearly any CFGA is the value of Future Cash Flows Discounted back to today (as long as Cash Flow Value is greater than Asset Value).

Now, going back to a point made in the First Article, you should always anchor back to the House analogy when you get stuck (especially in an interview!).

For all of my past students, a House is generally easier to think through conceptually than the more abstract concept of a ‘Business’…especially when you’re just beginning your Finance Learning Journey.

As mentioned at the beginning of the article, there are Two primary Business Valuation Methods: Intrinsic Valuation and Multiple-Based Valuation.

In Article #3, we’ll continue our discussion of common Business Valuation Methods with a similar walkthrough of Multiple-based Valuations. Stay tuned and hope to see you soon!

Please let us know if you have any comments or questions below.